Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.

This content is for educational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making financial decisions.

Can I Get Cash for My Structured Settlement?

Yes. You can get cash for your structured settlement payments through a court-approved sale to a purchasing company. Every state in the U.S. permits these transactions under the Structured Settlement Protection Act, and most cash-outs fund within 45 to 90 days of your first call. CSF can advance you cash before the hearing in many cases so you are not waiting empty-handed.

Cash for structured settlement payments works the same way whether you sell all of your payments, only some of them, or payments from a specific time window. Most of our customers choose a partial sale to access cash for a specific need without giving up their entire future income stream. We see partial sales most often for paying off high-interest debt, covering medical bills, buying a home, and funding education or a business.

How much cash you get depends on the dollar value of the payments you sell, how far in the future they are, and the discount rate applied. Sooner payments are worth more today than later payments. Get quotes from at least two or three companies before deciding. The amount we quote is the amount you receive at closing. Not a penny less. Call us at (800) 317-3769 or fill out the form on this page for a same-day quote. We go deeper on the math in our guide on how much you will get if you sell your structured settlement, and our overview of structured settlement buyouts covers the full-vs-partial sale decision and what the buyout actually costs.

What Does It Mean to Cash Out a Structured Settlement?

Cashing out a structured settlement means selling some or all of your future periodic payments to a purchasing company in exchange for a lump sum of cash through a court-approved process. The transaction requires a judge to review the terms and confirm the sale is in your best interest before any money changes hands.

Structured settlements were originally designed to provide long-term financial stability after a personal injury or wrongful death claim. The payments come from an annuity purchased by the defendant or their insurer, and they are typically tax-free under IRC Section 104(a)(2) (opens in a new tab). That tax-free status does not change when you sell.

The process is governed by the Structured Settlement Protection Act (SSPA), which exists in some form in every state. The SSPA requires court approval, written disclosures about the terms, and in most states, notice to the original parties in the settlement agreement. These protections exist to make sure no one sells payments without fully understanding what they are giving up.

If you are reading this, you are probably weighing whether selling makes sense for your situation. That is the right approach. Get quotes from at least two or three companies, compare the offers, and make sure you understand the difference between selling all of your payments and selling just some of them. Most of CSF's customers choose a partial sale.

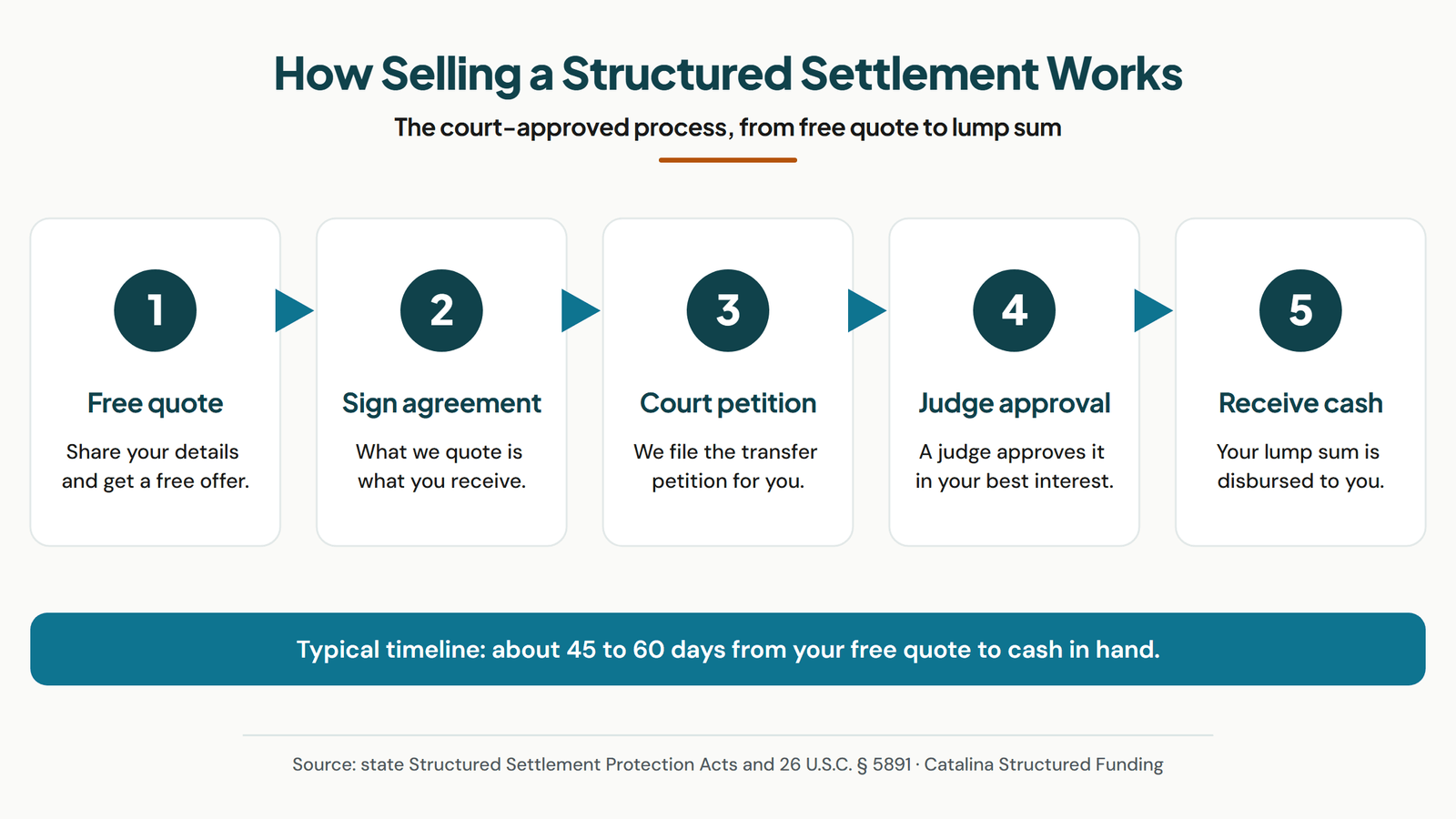

How to Cash Out Your Structured Settlement (Step by Step)

The structured settlement cash out process involves seven steps, from your initial quote through final funding, and most transactions reach court approval within 30 to 45 days of filing. Here is what each step looks like.

Step 1: Get a Quote

Call a purchasing company or fill out a form to get a lump sum offer based on your payment schedule. The company will ask for details about your annuity, including the payment amounts, dates, and issuer. At CSF, you can call us at (800) 317-3769 or fill out the form on this page. We provide quotes the same day.

Get quotes from at least two or three companies before making a decision. We say that because we know what happens when people compare. They usually come back to us.

Step 2: Review the Contract

Once you accept an offer, the company prepares a transfer agreement. This contract spells out exactly which payments you are selling, the lump sum amount you will receive, and the discount rate applied. Read it carefully. The amount on the contract should match the quote you were given.

At CSF, the amount we quote is the amount you receive. Not a penny less.

Step 3: Sign the Paperwork

You sign the transfer agreement, typically through DocuSign or with a notary. CSF handles everything electronically when possible so you do not have to leave your house. After signing, you receive written disclosure documents that explain the financial impact of the sale, including the difference between the total value of your remaining payments and the lump sum amount.

Step 4: Court Filing

CSF files a transfer petition with the court in your jurisdiction. Most states require a 20-day notice period after the petition is filed. CSF files for the soonest available hearing date after that period expires. Courts in states like Illinois and Louisiana have approved transactions in as few as 20 to 25 days from the date of filing. Most states schedule hearings within 30 to 45 days.

Step 5: Independent Professional Advice

Most states require that you be advised of your right to seek independent professional advice (IPA) before the hearing. The IPA is typically a licensed attorney or financial planner who reviews the terms and advises you on whether the sale makes sense for your situation. CSF covers the cost of this advisor.

Step 6: Court Hearing

A judge reviews the transaction at a scheduled hearing. The hearing typically takes about 20 minutes. The judge confirms you understand what you are giving up, verifies that you received proper disclosures, and determines whether the transfer is in your best interest. Most hearings are routine. Many courts allow you to attend remotely by Zoom, phone, or video at the judge's discretion.

Step 7: Court Approval and Funding

After the judge signs the order approving the transfer, CSF sends the order to the annuity issuer for acknowledgment. Funding can happen as quickly as one business day after the issuer processes the paperwork. Any delays at this stage are typically caused by the clerk's office processing the signed order or missing underwriting items.

Need cash before court approval? CSF offers cash advances on pending transactions. We can advance you money the same day you sign your contract, so you are not stuck waiting while the paperwork moves through the court.

Cash Out vs. Cash Advance: What Is the Difference?

A structured settlement cash out is a permanent sale of future payments, while a cash advance is early access to money from a pending transaction that has not yet been approved by the court. They serve different purposes and work on different timelines.

We see confusion between these two terms regularly. Here is a clear breakdown.

| Feature | Cash Out (Sell Payments) | Cash Advance |

|---|---|---|

| What it is | Permanent sale of future payments for a lump sum | Early access to money from a pending sale |

| Court approval required | Yes, always | No (advance is issued before court hearing) |

| Timeline | 30 to 60 days | Same day or next business day |

| Effect on your payments | Sold payments are permanently transferred | Deducted from your final payout at closing |

| When to use | When you need a large lump sum | When you need cash before court approval |

| Additional cost | Discount rate applied to present value | Advance fee deducted at closing |

The short answer is that a cash out is the transaction itself, and a cash advance is a bridge to help you get through the waiting period. Say your offer is $38,000 and you take a $3,000 cash advance up front. At closing, you receive the remaining $35,000. The advance is not extra money. It is early access to money that is already yours.

We go deeper into how structured settlement cash advances work, including how much you can expect and how fast the money arrives.

Can You Cash Out Part of Your Structured Settlement?

Yes, you can sell a portion of your structured settlement payments while keeping the rest of your payment schedule intact. Most of CSF's customers choose a partial sale rather than selling everything.

There are three common ways to structure a partial sale, and the right one depends on how much cash you need and how much income you want to keep.

1. Sell a Block of Payments

You sell a specific number of payments from the beginning of your schedule. For example, if you receive $2,000 per month and you sell the next 36 months of payments, you give up $72,000 in future payments and receive a lump sum based on the present value of those payments. After 36 months, your remaining payments resume as scheduled.

2. Sell a Percentage of Each Payment

You sell a portion of every payment rather than all of any single payment. For example, you might sell 50% of each $2,000 monthly payment for the next five years. You continue receiving $1,000 per month during that period, and you get a lump sum for the other half. This structure works well for people who need cash but also rely on their settlement for monthly expenses.

3. Sell Payments from a Specific Date Range

You sell only the payments that fall within a specific window. For example, you might sell all payments between January 2028 and December 2030, keeping everything before and after that range. This gives you cash now while preserving your near-term income and your long-term payments.

This sounds more complicated than it actually is. CSF walks you through the options and helps you figure out which structure puts the most cash in your pocket without giving up more than you need to. Call us at (800) 317-3769 and we will go through your payment schedule together.

Want to know what your payments are worth?

The fastest way to find out is to call us at (800) 317-3769 or fill out the form on this page. There is no cost, no obligation, and no pressure.

What Do People Use the Cash For?

The most common reason people cash out a structured settlement is to buy a home or cover housing costs, followed by paying off debt and purchasing a vehicle. Here is what CSF's transaction data shows.

Based on CSF's review of court filings from thousands of completed transactions, the top reasons customers sell their structured settlement payments are:

- Home purchase or housing costs: 44% of transactions

- Debt payoff: 25% of transactions

- Vehicle purchase: 11% of transactions

- Business investment or startup: 6% of transactions

- Other (education, medical, relocation): 14% of transactions

Nearly half of CSF's customers use their lump sum to buy a home or make a down payment. That tracks with what we hear on the phone every day. People are tired of renting, and they have $200,000 or more sitting in future payments they cannot touch. A partial sale can unlock the down payment without wiping out their entire settlement.

The second biggest category is debt payoff. We see people carrying $15,000 to $40,000 in credit card debt at 20% to 28% interest. Selling $25,000 in future payments to eliminate that debt can save thousands in interest over the next several years. The math usually works in the seller's favor.

Courts do not generally require you to justify your reason for selling, but the judge may ask. Having a clear plan for the money helps the process go smoothly.

How to Choose a Company to Cash Out With

The best way to choose a structured settlement purchasing company is to get quotes from at least two or three companies, compare the lump sum amounts, and ask whether the company is the buyer or a lead generator. Lead-generation sites collect your information and pass it to other companies for a referral fee. The company you sell to should be the company that quoted, signed, and closed the deal.

CSF has closed more than 4,000 transactions since 2011 and funds quotes from our own capital. Your timeline does not depend on a separate party approving the deal after you sign.

When you are comparing companies, ask these questions:

- Is the lump sum amount guaranteed in writing, or can it change before court?

- Does the company handle the court filing and hearing, or do you need to hire your own attorney?

- How long has the company been in business, and is it registered in your state?

- Does the company offer cash advances while you wait for court approval?

- What is the company's BBB rating and review history?

We encourage comparison shopping because we know what happens when people compare. They usually come back to us. We go deeper into the differences between companies in our structured settlement companies comparison.

What Issuers Can You Cash Out From?

You can cash out a structured settlement from any annuity issuer, regardless of which insurance company holds your annuity contract. The issuer does not have the right to block a court-approved transfer.

CSF has processed transactions involving American General/Corebridge (400+), MetLife (390+), Prudential (345+), and every other major issuer. We have worked with Allstate/Everlake, John Hancock, Talcott Resolution (formerly Hartford), New York Life, Symetra, GABC, Genworth, Pacific Life, Transamerica, and dozens of others.

Each issuer has its own internal process for acknowledging transfers. Some move quickly. Others take longer. We know their timelines, their paperwork requirements, and which contact numbers actually get you to the right department. That experience matters because delays at the issuer level are the most common cause of funding holdups after court approval.

You can find issuer-specific transfer guides on our annuity issuers page, including Verification of Benefits (VOB) instructions for each company.

Frequently Asked Questions

Can I get cash for my structured settlement?

How fast can I get cash for my structured settlement payments?

How long does it take to cash out a structured settlement?

Can I cash out only part of my structured settlement?

Do I need a lawyer to cash out my structured settlement?

Will cashing out my structured settlement affect my taxes?

What is the difference between cashing out and getting a cash advance?

Can I cash out my structured settlement if I have sold payments before?

How much cash will I get for my structured settlement?

Will I get cash for my structured settlement payments tax-free?

What happens at the court hearing for a structured settlement cash out?

Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.