Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.

This content is for educational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making financial decisions.

Can You Sell a Structured Settlement?

Yes. Every state in the U.S. permits the sale of structured settlement payments through a court-approved transfer. The process is governed by the Structured Settlement Protection Act (SSPA), which exists in some form in every state and requires a judge to review the terms of the sale and confirm it is in your best interest before the transfer is complete.

Structured settlements were originally designed to provide long-term financial stability after a personal injury or wrongful death case. The payments come from an annuity that was purchased as part of the settlement, and they are typically tax-free under IRC Section 104(a)(2). That tax-free status does not change when you sell.

You can sell all of your remaining payments, only some of them, or payments from a specific time window. Most of our customers choose a partial sale because it gives them cash now without giving up their entire future income stream. We go deeper on the partial-sale option in our guide on selling part of your structured settlement, and our companion overview of structured settlement buyouts covers what the buyout actually costs and when it makes sense.

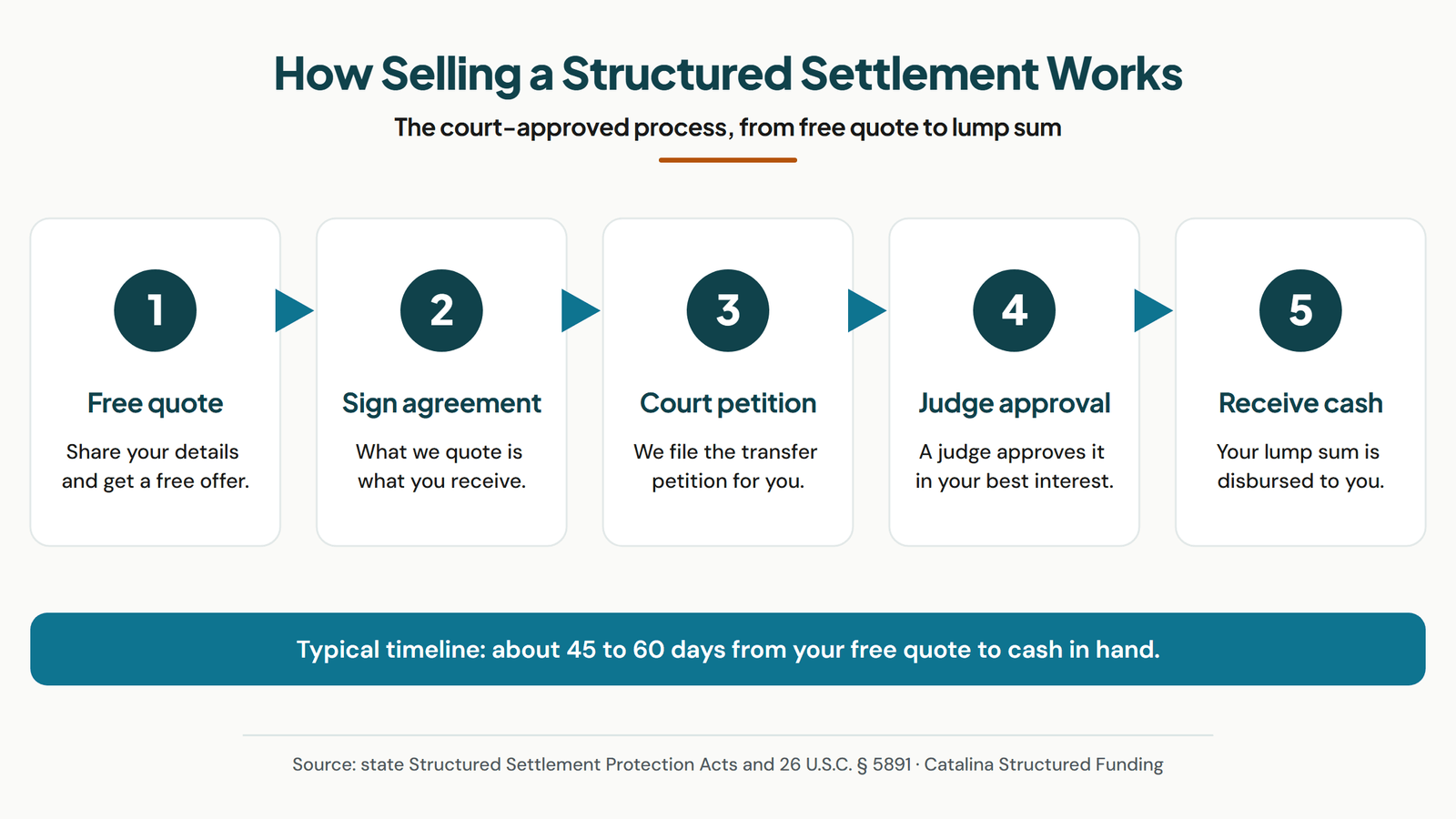

How to Sell a Structured Settlement (Step by Step)

Selling a structured settlement is a seven-step process from your first quote to the day the lump sum hits your bank account. Most sales fund in 45 to 90 days. Here is what each step looks like.

Step 1: Get a Quote

Call us at (800) 317-3769 or fill out the form on this page with the basics of your payment schedule: the issuer, payment amounts, dates, and how much cash you need. We provide quotes the same day. Get quotes from at least two or three companies before you accept one. We say that because we know what happens when people compare. They usually come back to us.

Step 2: Review the Offer

The quote breaks down which payments you would be selling, the lump sum amount, and the discount rate applied. Read it carefully and ask questions. The amount we quote is the amount you receive at closing. Not a penny less.

Step 3: Sign the Transfer Agreement

Once you accept, you sign a transfer agreement, usually electronically through DocuSign. We handle the paperwork remotely whenever possible so you do not have to leave your house. After signing, you receive written disclosure documents that explain the financial impact of the sale, including the difference between the total value of the payments and the lump sum.

Step 4: We File the Petition

CSF files a petition with the appropriate court in your state. The petition includes your transfer agreement, the disclosures, and a request for a hearing date. Most courts schedule the hearing 30 to 45 days after filing. We have dealt with every major annuity issuer, including MetLife, Prudential, and New York Life, and we coordinate directly with them on the acknowledgment and notice requirements.

Step 5: The Court Hearing

The hearing usually takes about 20 minutes. The judge reviews the terms of the sale, confirms you understand what you are giving up, and verifies the transfer is in your best interest. Most courts allow you to attend by phone or video at the judge's discretion. The judge applies a state-specific best-interest standard that considers your financial situation, your reason for selling, and whether the proposed terms are fair.

Step 6: The Order Issues

After the hearing, the judge signs an order approving the transfer. The clerk issues a file-stamped copy, which we send to your annuity issuer along with the transfer paperwork. The annuity issuer redirects the payments you sold to CSF.

Step 7: Funding

Once the issuer acknowledges the order and underwriting is clear, we wire your lump sum to your bank account, typically within one business day of receiving the signed order. Funding can also be issued by check or ACH if you prefer.

How to Get a Structured Settlement Quote

A structured settlement quote is the buyer's written offer for some or all of your future payments. Every state requires the buyer to provide it in writing on a disclosure statement before you sign anything. Verbal quotes are a starting point, not a number you can compare. The eight steps below take you from your first phone call through the written quote you should expect from any reputable buyer. For a deeper walkthrough on how to get a structured settlement quote and how to compare offers, that page covers what should be in every quote and what red flags to watch for.

- Submit your payment details. Most buyers ask for the payment amount, payment frequency, payment start and end dates, the annuity issuer, and whether the payments are guaranteed or life-contingent.

- Receive a preliminary verbal quote. Within 24 hours you should have a ballpark net lump sum. Treat this as a screening number, not a commitment from either side.

- Request the written disclosure. The disclosure is the binding number. It must show the gross purchase price, the discount rate, every cost being deducted, and the net lump sum you will receive at funding.

- Confirm exactly which payments you are selling. A buyer who quotes “your settlement” without itemizing payments by date and amount is leaving themselves room to swap the math later. Pin it down in writing.

- Send the disclosure to a comparable buyer. Get at least one independent quote on the same payment stream. We see 5+ percentage point spreads in discount rate on identical deals.

- Sign the purchase agreement. Once you have chosen a buyer, sign the disclosure + purchase agreement. The clock to court approval starts here.

- Buyer files the petition; court reviews; judge approves. The petition is filed within a few days; the court schedules a hearing 30 to 60 days out depending on the state and county.

- Funds release after the judge signs the order. One to three business days from the signed order to wire is typical when underwriting is clean. Some states add an acknowledgment step on top of that.

Five questions to ask any buyer before you sign the disclosure:

- What is the net lump sum I will receive? Not the gross. The actual amount that hits my account on funding day.

- What is the discount rate, in writing? Every state requires the rate on the disclosure. If a buyer will not put it on paper, walk away.

- Are court costs, attorney fees, IPA fees, or processing costs deducted from my net? Some buyers absorb these. Others do not. Ask explicitly.

- Are you the buyer, or are you passing my information to other companies? The company you sell to should be the company that quoted, signed, and closed the deal — not a referral site that handed your details to multiple funders for a fee. CSF quotes, signs, and closes our own transactions with capital on hand.

- What entity will sign the purchase agreement? If the entity is one of the 18 in The J.G. Wentworth Company family of companies, you are getting a JGW quote even if the brand name on the page is Peachtree, Stone Street, or Settlement Funding LLC. Compare a JGW family quote against an independent buyer, or read our direct Peachtree vs. CSF comparison.

Have a quote in hand and want to compare it? Call us at (800) 317-3769 or request a written CSF quote on this page. The amount we quote is the amount you receive.

How Much Will I Get if I Sell My Structured Settlement?

The short answer is that you will receive less than the total face value of the payments you sell, because money you would receive years from now is worth less today. The amount depends on four variables.

- The total dollar value of the payments you are selling

- The timing of those payments. Sooner payments are worth more today than later payments.

- The discount rate, which reflects the time value of money and is the single biggest driver of your payout

- Whether the payments are guaranteed or life-contingent. Life-contingent payments (those that stop at your death) are priced differently than guaranteed payments

Discount rates are set per-transaction based on current market rates and the structure of your payment schedule. We will be transparent about ours and explain how it was calculated.

We go deeper on the math in our guide on how much you will get if you sell your structured settlement, including worked examples for different payment structures and timeframes.

Should I Sell My Structured Settlement?

Selling makes sense when you have a use for the cash that beats the long-term value of keeping the payments. We see four scenarios most often.

Buying or keeping a home is the most common reason, accounting for roughly 44 percent of CSF transactions. Customers use the lump sum for a down payment, a major renovation, or to pay off a remaining mortgage balance. Paying off high-interest debt is the second most common reason at about one in four transactions. If you are paying 22 percent APR on a credit card while your settlement delivers a 4 to 5 percent effective return, the math often favors a lump-sum payoff. Buying a reliable vehicle, starting or investing in a business, and covering personal needs round out the typical reasons. We cover the math and the trade-offs for each in detail in our guides on selling to buy a house, selling to pay off debt, and selling to buy a car.

Selling does not make sense in two situations. If you have no specific plan for the cash, you are likely better off keeping the payments. And if your monthly settlement payment is your only income covering essential expenses, you should consider a partial sale rather than a full sale.

Talk to a financial advisor or attorney before you decide. State law requires you to be advised of your right to seek independent professional advice before the court hearing, and CSF covers the cost of that advisor as part of the transaction. Our full decision guide on whether you should sell your structured settlement walks through the five scenarios where selling makes sense, the three where it does not, and the effective-interest-rate math behind each.

Sell All or Sell Part: Which Is Right for You?

Most of our customers sell only part of their structured settlement. A partial sale gives you cash now while preserving long-term income. There are three common partial-sale structures.

- Sell a specific number of future payments. For example, sell the next 36 monthly payments and keep everything after that

- Sell a portion of each payment. For example, sell half of every monthly payment and keep the rest

- Sell payments from a specific window. For example, sell the payments scheduled between 2030 and 2035 and keep all others

The legal process is the same as a full sale, and the tax-free status of the payments you keep is preserved. We see partial sales work especially well for customers who want to cover a one-time expense without giving up their long-term income safety net. Our blog post on partial sales walks through specific structures and which one fits different situations.

Why Sellers Choose CSF

We have closed more than 4,000 structured settlement transactions since 2011. We consistently beat competing offers, and we have a track record to prove it. Our team includes licensed attorneys who handle every aspect of the transfer, from the petition through the final order. You do not need to hire your own lawyer.

We have dealt with every major annuity issuer in the industry. We know their internal timelines, their paperwork requirements, and which ones move fastest. That experience matters when small mistakes on the issuer side can add weeks to your timeline. We catch them before they happen.

Our pricing is transparent. The amount we quote is the amount you receive at closing. We will explain how we arrived at the discount rate so you can compare apples to apples with other companies. If a competitor offers more, tell us. We want to earn your business.

We can advance you cash before the court hearing in many cases through our cash advance program, so you are not waiting empty-handed during the 45 to 90 day approval window. The advance is not extra money. It is early access to money that is already yours, deducted from your final payout at closing.

Compare Companies Before You Sign

Get quotes from at least two or three structured settlement buyers before you commit. Brand recognition is not the same as the best payout, and the difference between a good offer and a bad one is often tens of thousands of dollars on the same payment stream. Our guide to the best structured settlement companies walks through how to evaluate buyers on discount rate, in-house legal capability, BBB rating, and customer service. For a tighter overview focused specifically on structured settlement buyers and how to choose one, that page distills the same evaluation into one read.

Have questions about what your payments are worth? Call us at (800) 317-3769. That gets you a direct line to our team, not a call center. There is no cost, no obligation, and no pressure.

Frequently Asked Questions

Can you sell a structured settlement?

Yes. State law in every U.S. state permits the sale of structured settlement payments through a court-approved transfer process. The Structured Settlement Protection Act, in some form in every state, governs these sales and requires a judge to confirm the transaction is in your best interest before any money changes hands. Most sales close within 45 to 90 days of filing.

How do I sell my structured settlement?

The process is seven steps. You request a quote, accept an offer, sign a transfer agreement, receive written disclosures, file a petition with the court in your state, attend a short hearing, and receive your lump sum after the judge signs the order. CSF handles every filing and coordinates directly with your annuity issuer. You typically only need to show up for the hearing, which is often available by phone or video.

How much will I get if I sell my structured settlement payments?

The lump sum depends on the dollar value of the payments you sell, how far in the future they are, the discount rate applied, and whether the payments are guaranteed or life-contingent. Sooner payments are worth more than later ones because of the time value of money. Get a quote from at least two or three companies before deciding. We go deeper on what affects your payout in our guide on how much you can expect to receive.

Can I sell part of my structured settlement instead of all of it?

Yes, and most of our customers do. A partial sale lets you take cash from a specific number of payments, a slice of each payment, or payments from a specific time window, while keeping the rest of your income intact. A partial sale is the same legal process as a full sale and the tax-free status of your remaining payments is preserved.

How long does it take to sell a structured settlement?

Most sales fund in 45 to 90 days from your first call. Courts in some states have approved transfers in as few as 20 to 25 days from filing. The timeline depends on your state's court calendar, the speed of the annuity issuer's acknowledgment, and how quickly paperwork moves through underwriting. CSF can advance you cash before the hearing in many cases so you are not waiting empty-handed.

Should I sell my structured settlement?

Selling makes sense when you have a use for the cash that beats the long-term value of holding the payments. We see customers sell to pay off high-interest debt, cover medical bills, buy a home, fund a business, or pay for education. Selling does not make sense if you have no specific use for the cash or if your monthly payments are the only income covering essential expenses. Talk to a financial advisor or attorney before deciding.

Will I have to pay taxes if I sell my structured settlement payments?

If your structured settlement payments are tax-free under IRC Section 104(a)(2) because they originated from a personal physical injury or sickness claim, the lump sum you receive is also tax-free. The tax-free status survives the sale. If your payments come from a non-qualified settlement (employment claims, defamation, certain commercial cases) the tax treatment is different and you should consult a tax professional.

Do I need a lawyer to sell my structured settlement?

You are not required to hire your own attorney. State law requires that you be advised of your right to seek independent professional advice from a licensed attorney or financial planner before the court hearing, and CSF covers the cost of that advisor as part of the transaction. CSF's in-house legal team handles every court filing and disclosure document for you.

Can I sell my structured settlement if I have sold payments before?

Yes. Many of our customers have completed prior transactions with other companies. You can sell additional payments from your remaining schedule. The court reviews each new transaction on its own merits, including whether the sale is in your current best interest. Prior sales do not disqualify you.

Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.

Ready to See What Your Payments Are Worth?

The fastest way to find out is to call us at (800) 317-3769 or fill out a quote request. Same-day quotes, free, with no obligation. We are licensed in every state where structured settlement transfers are permitted.