Sell Your Structured Settlement for a Lump Sum (2026)

If you need cash now, you can sell some or all of your future payments for a lump sum. CSF handles the court filings, the paperwork, and the coordination with your insurance company. Rene sold her annuity payments with CSF and bought her first home in about two months. Free quote, no obligation, nationwide.

How the Process Works

Get a Free Quote

Tell us about your payments. We’ll provide a competitive lump sum offer within 24 hours.

Court Approval Process

CSF handles all legal filings, paperwork, and court scheduling on your behalf at no cost.

Receive Your Lump Sum

After court approval (typically 30–60 days), your funds are transferred directly to you.

Reviewed by Chris M., Esq., President, CEO & Founder | Licensed in Florida

Last updated:

Selling a structured settlement is a court-approved transaction in which a purchasing company pays you a lump sum of cash in exchange for some or all of your future periodic payments. If you are receiving structured settlement payments and need that money sooner, you can sell through a process governed by your state's Structured Settlement Protection Act (SSPA). The process typically takes 30 to 60 days from first call to funding. If you are still learning the basics, our plain-English guide to what a structured settlement is explains how these payment streams are created and taxed.

Most of our customers start right where you are: the payment schedule that made sense years ago does not match your life today. Catalina Structured Funding has closed more than 4,000 structured settlement transactions. We handle the court filing, the paperwork, and the coordination with your annuity issuer. The amount we quote is the amount you receive. Not a penny less.

What Is a Structured Settlement?

A structured settlement is a financial arrangement in which compensation from a lawsuit is paid out as a series of periodic payments over time, rather than as a single lump sum. These payments are funded through an annuity purchased from a life insurance company (such as MetLife, Prudential, or New York Life) on behalf of the defendant. The National Structured Settlements Trade Association (NSSTA) (opens in a new tab) maintains a comprehensive overview of how these arrangements are established.

Structured settlements most commonly arise from personal injury, workers' compensation, medical malpractice, wrongful death, and wrongful imprisonment cases. They are also frequently used for settlements involving minors. Once established, the insurance company makes payments directly to you according to the schedule outlined in the agreement.

If your case has not settled yet and you need funds now, our guide to pre-settlement funding explains how that process works and how it compares to selling structured settlement payments after a case closes.

Why People Sell Structured Settlements

If you are reading this, you have probably been thinking about selling your payments for a while. Most of our customers start where you are right now. The payment schedule that made sense years ago does not match your life today.

Across more than 4,000 closed CSF transactions, the reasons cluster in a clear order. About 44 percent of our customers sell to buy or keep a home: a down payment, a renovation, or paying off a mortgage. Roughly one in four sells to pay off debt, usually high-interest credit cards or personal loans. Vehicle purchases, business investments, and other personal needs round out the rest. Medical bills are an occasional reason but a small share. Whatever the reason, CSF does not require you to justify your decision.

- Buying a home or paying off a mortgage, including down payments and home renovations

- Paying off high-interest debt like credit cards or personal loans

- Buying a reliable vehicle or replacing a vehicle that is failing

- Starting or investing in a business

- Funding education for yourself or your children

- Covering medical expenses or long-term care costs

You do not have to sell all of your payments. You can sell a specific number, payments from a defined time period, or a portion of each payment while keeping the rest. Our guide on how to sell your structured settlement walks you through the full process, and our structured settlement company comparison can help you evaluate which buyer is the right fit.

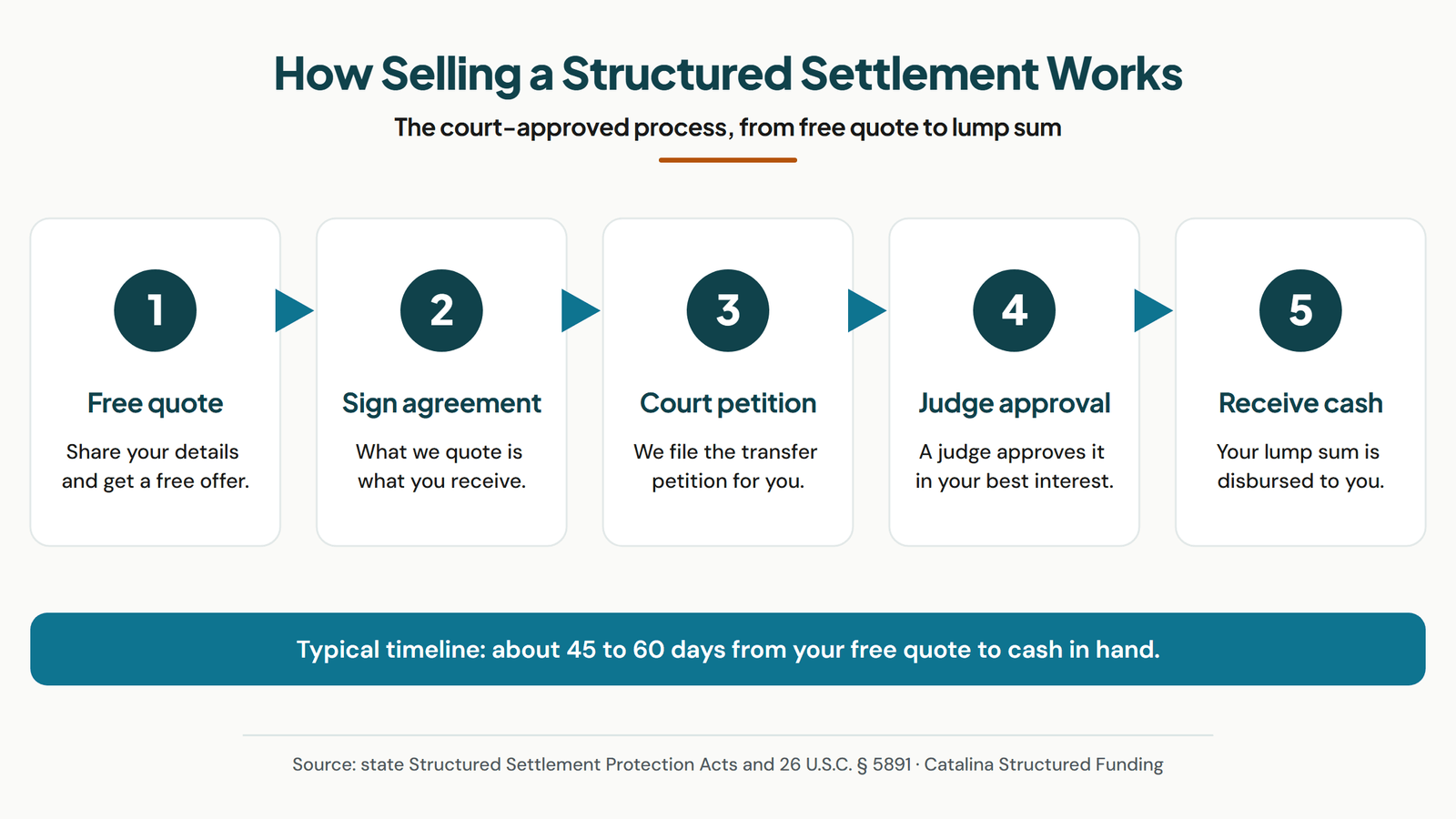

How to Sell Your Structured Settlement

Selling structured settlement payments is a legal process governed by your state's Structured Settlement Protection Act (SSPA). The National Structured Settlements Trade Association (NSSTA) (opens in a new tab) provides additional background on how these laws work. Every state requires court approval, and that requirement exists to protect you. Here are the steps from first call to funding.

- Get a free quote. Call CSF or fill out the form on this page with the basics about your payments. We will have a lump-sum offer to you within 24 hours. No obligation.

- Review and accept the offer. CSF prepares all required legal documents: the purchase agreement, the disclosure statement, and the court petition. You review and sign.

- Notice period and court filing. CSF files the petition with the court and sends notice to all interested parties, including the annuity issuer and in some states the attorney general. The notice period runs 20 to 30 days.

- Court hearing and approval. A judge reviews the transaction during a short hearing, usually 15 to 45 minutes. The judge confirms the sale is in your best interest and that you were not pressured. CSF handles scheduling and logistics.

- Transfer and funding. After the judge signs the court order, funding can happen as quickly as one business day if all underwriting items are complete. Minor delays may occur if the judge takes a few days to sign the order, the clerk is slow to provide a file-stamped copy, or you still need to submit required paperwork (such as annuity contract documents). Total timeline: 30 to 60 days.

Most courts require a 20-day notice period before the hearing. CSF files for the soonest available hearing date after that notice period expires, which is why most of our transactions close in 30 to 60 days. This sounds more complicated than it actually is. Most customers do not have to do much beyond signing paperwork and showing up to the hearing. If you need cash before the court date, we offer cash advances on pending transactions. We cover the full timeline in our guide on how long it takes to sell a structured settlement.

How Much Can You Get for Your Structured Settlement?

The lump sum you receive depends on the total remaining value, payment schedule, payment type, issuing insurance company, and current market conditions.

We see sellers with nearly identical face values walk away with very different lump sums. The reason is that no two structured settlements are alike. A settlement paying $2,100 per month for 15 years looks different from one paying $8,500 annually with a $75,000 lump sum in 2031. The payment structure shapes the offer just as much as the dollar amount.

Here is a realistic example. Say you have $124,000 in total remaining payments spread across monthly installments over the next 12 years. A structured settlement buyer applies a discount rate to calculate the present value of those future payments. In that scenario, you might receive a lump sum offer of $68,000 to $81,000 depending on the rate. The gap between a competitive offer and an average one can be $13,000 or more on a single transaction.

Five factors drive the number you see on your quote:

- Total remaining payments. The more future value on the table, the larger the lump sum.

- Payment schedule. Monthly payments that start immediately are worth more than annual payments that begin five years from now. Payments closer to today carry more present value.

- Guaranteed vs. life contingent. Guaranteed (period certain) payments receive stronger offers because the buyer is not taking on actuarial risk. Life contingent payments are still sellable, but the pricing reflects the added uncertainty.

- Issuing insurance company. Annuity issuers like MetLife, Prudential, and Corebridge each have their own transfer timelines and paperwork requirements. Some move faster than others, and that can affect the offer.

- Current market conditions. Interest rates and the broader financial environment influence discount rates across the industry. When rates shift, so do lump sum offers.

The best way to know what your payments are worth is to get a quote. Our structured settlement calculator gives you a general idea, and a phone call gets you a real number. Get quotes from at least two or three structured settlement companies before making a decision. We say that because we know what happens when people compare. They usually come back to us.

What Is a Discount Rate?

A discount rate is the percentage a structured settlement buyer uses to calculate the present value of your future payments and determine your lump sum offer.

The concept comes down to the time value of money. A dollar you receive today is worth more than a dollar you receive ten years from now. You could invest that dollar today, earn a return on it, or simply use it to cover expenses that are costing you money right now. The discount rate puts a number on that difference.

In the structured settlement industry, discount rates typically range from 9% to 18%, according to the National Structured Settlements Trade Association (NSSTA) (opens in a new tab). The lower the rate, the more cash you receive. A buyer offering a 10% rate on the same payment stream will pay you significantly more than a buyer at 16%. That spread is why comparison shopping matters so much in this industry.

CSF consistently offers discount rates at the competitive end of that range. We are not the only company that claims to beat the competition, but we welcome the comparison. If you already have a quote from another structured settlement buyer, share it with your CSF representative and give us the chance to beat it. Call us at (800) 317-3769 to get a direct line to our team, not a call center. We go deeper into how discount rates work and what affects them if you want to understand the math before calling.

Structured Settlement Sale vs. Structured Settlement Loan

A structured settlement sale is a one-time transaction where you sell future payments for a lump sum, while a structured settlement loan uses your payments as collateral for a debt you must repay with interest.

We see this confusion constantly. People search for "structured settlement loan" when what they actually want is to sell their payments outright. The distinction matters because the two options have completely different financial consequences.

When you sell your structured settlement payments through CSF, you receive a lump sum and you are done. There are no monthly payments to make, no interest accumulating, and no risk of default. The court approves the transaction under your state's Structured Settlement Protection Act (SSPA), and the money is yours to use however you choose.

A loan against your structured settlement is a different product entirely. A lender gives you cash now, and you repay it with interest out of your future payments. If you miss payments, the lender can pursue collection. Your credit score is on the line. And the total cost of the loan (principal plus interest) often exceeds what you would have given up by selling outright.

| Factor | Structured Settlement Sale | Structured Settlement Loan |

|---|---|---|

| How it works | You sell future payments for a lump sum | You borrow against future payments and repay with interest |

| Monthly payments after | None | Yes, until the loan is repaid |

| Interest charges | None (a discount rate is applied, not interest) | Yes, often at high rates |

| Court approval required | Yes, under your state's SSPA | Varies by lender and state |

| Credit check | May be required | Typically required |

| Risk of default | None (transaction is final) | Yes, missed payments can lead to collections |

| Tax treatment | Generally tax-free for personal injury under IRC 104(a)(2) (opens in a new tab) | Loan proceeds are not taxable, but interest is not deductible |

| Impact on remaining payments | Sold payments stop; unsold payments continue | All payments continue, but a portion goes to repayment |

Most people who come to us looking for a "structured settlement loan" end up choosing a sale once they understand the difference. A sale is cleaner, court-supervised, and final. You walk away with your lump sum and no ongoing obligation. If you want to keep some of your payments, you do not have to sell everything. You can sell a specific number of payments or a portion of each payment and keep the rest.

What Types of Structured Settlements Can You Sell?

You can sell structured settlement payments from personal injury, workers' compensation, wrongful death, medical malpractice, and wrongful imprisonment cases.

The type of case that created your settlement does not change the selling process much. The court still reviews the transaction under your state's SSPA. The judge still confirms the sale is in your best interest. What does change is whether the payments are guaranteed or life contingent, and that distinction directly affects your offer.

Common Case Types

- Personal injury. The most common type we see. Auto accidents, slip-and-fall cases, product liability claims. Payments from personal physical injury settlements are generally tax-free under IRC 104(a)(2), and that tax treatment carries over to the lump sum.

- Workers' compensation. Many workers' comp settlements are structured into periodic payments. State laws vary on whether these can be transferred. We cover the details in our workers' comp settlement guide.

- Wrongful death. Surviving family members who receive structured settlement payments from a wrongful death claim can sell those payments through the same court-approved process.

- Medical malpractice. These settlements often involve large payment streams funded by insurers like New York Life or Corebridge. The transfer process is the same, though some issuers have specific paperwork requirements.

- Wrongful imprisonment. Exonerees who received structured settlement payments as part of their compensation can sell some or all of those payments. These cases sometimes involve state-funded annuities with unique terms.

Guaranteed vs. Life Contingent Payments

The type of payments you have directly affects what a buyer can offer. There are two main categories, and many settlements include both.

Guaranteed payments (also called "period certain" payments) are paid for a fixed number of years regardless of whether the payee is alive. If you pass away during the guaranteed period, a designated beneficiary continues to receive the remaining payments. These are the most straightforward to sell and typically receive the strongest offers relative to their face value. We cover what happens in that scenario in our guide on structured settlements after death.

Life contingent payments continue only as long as the measuring life (usually the payee) is alive. When the measuring life passes away, payments stop. No residual value goes to beneficiaries. Many settlements include both a guaranteed period followed by a life contingent phase.

We see a lot of confusion around life contingent payments. Many companies will not purchase them because the buyer takes on actuarial risk. CSF specializes in these transactions. We have dealt with every major annuity issuer, including MetLife, Prudential, and New York Life, and we know how to price them competitively. Our life contingent payments guide explains the valuation in detail.

Common Mistakes When Selling a Structured Settlement

The most common mistake is accepting the first offer without getting a second quote, which can cost you thousands of dollars on a single transaction.

We see the same patterns over and over. After closing more than 4,000 structured settlement transactions, we know exactly where sellers lose money or get tripped up. Here are the mistakes we see most often.

Accepting the first offer without comparing

This is the single biggest mistake, and we see it constantly. The difference between a competitive offer and a mediocre one can be $8,000 to $15,000 on a mid-sized transaction. Some companies count on sellers not shopping around. Get quotes from at least two or three structured settlement companies before signing anything. We encourage it because we know where we stand.

Not reading the disclosure statement

Your state's SSPA requires every structured settlement buyer to provide a written disclosure statement before you sign the purchase agreement. This document spells out the discount rate, the total amount you are giving up, and the net amount you will receive. We see sellers who sign without reading it and then feel surprised at closing. Read every line. If something is unclear, ask your buyer to explain it. At CSF, we walk every customer through the disclosure in plain language.

Selling more payments than you need

You do not have to sell all of your payments. We see sellers who cash out their entire payment stream when they only needed $25,000 for a medical bill. You can sell a specific number of payments, a defined time period, or a portion of each payment. A partial sale keeps some of your future income intact while still putting cash in your hands today.

Not asking about cash advances

The court approval process takes 30 to 60 days. If you need money before the hearing, ask whether your buyer offers cash advances on pending transactions. Not every company does. CSF provides cash advances to nearly every customer, often the same day you accept an offer. The advance is not extra money. It is early access to money that is already yours.

Working with a lead-generation site instead of an actual buyer

Some sites that advertise as structured settlement buyers are actually lead-generation referral sites. They collect your information and pass it to multiple companies that pay for the referral. CSF quotes, signs, and closes our own transactions. We fund quotes from our own capital and work with an established network of financial partners, so your timeline does not depend on a separate party approving the deal after you sign. Ask any company you speak with: "Are you the buyer who will sign my purchase agreement, or are you passing my information to other companies?"

Avoiding these mistakes does not take much extra effort. A second phone call, a careful read of your disclosure, and the right questions can put thousands of additional dollars in your pocket.

How to Get Cash for a Structured Settlement

Cash for a structured settlement comes from selling some or all of your future payments to a licensed purchasing company through a court-approved transfer. The lump sum arrives 30 to 60 days after you accept an offer, and the buyer files the petition, handles the disclosures, and coordinates the court hearing in your state. Our dedicated guide on cash for structured settlement payments walks through the full process, partial vs. full cash-out structures, and how fast the money can reach you. If you are ready to sell your structured settlement payments, our LP covers the quote, court approval, and funding steps end to end.

If you have been searching for a way to turn your structured settlement into a lump sum, the process is more straightforward than most people expect. Every state has a Structured Settlement Protection Act (SSPA) that governs how these transactions work, and the law is designed to protect you at every step. Based on more than 4,000 completed transactions since 2011, here is what the process looks like in practice.

- Get quotes from multiple companies. Call at least two or three structured settlement buyers and compare lump sum offers. You want a direct funder, not a broker. Share basic details about your payment schedule and you should have an offer within 24 hours.

- Compare offers and ask questions. Look at the discount rate, the net amount you will receive, and whether the company charges anything beyond the discount. Ask each company if they are a direct funder or a broker. Ask about cash advances on pending transactions.

- Sign the purchase agreement and disclosure statement. Once you choose a buyer, you will sign a purchase agreement and a state-mandated disclosure statement that spells out every number. Read the disclosure carefully. At CSF, we walk every customer through it line by line.

- Court filing and notice period. Your buyer files a petition with the local court and notifies all interested parties, including the annuity issuer. Most states require a 20-day notice period before the hearing can be scheduled.

- Court approval and funding. A judge reviews the transaction at a short hearing and confirms the sale is in your best interest. After the judge signs the order, funding follows. In our experience filing in courts across the country, we have seen transactions approved in as few as 20 to 25 days in states like Illinois, Louisiana, and Georgia. Most states schedule hearings within 30 to 45 days of filing.

Those timelines are court approval dates, not funding dates. After the judge signs the order, it typically takes one to three business days for funds to arrive, assuming all underwriting items are complete. Some delays happen when a clerk is slow to provide the file-stamped order or when the seller still needs to submit annuity contract documents.

If you need cash before the court hearing, CSF offers cash advances on pending transactions, often the same day you accept an offer. The advance is not extra money. It is early access to money that is already yours. Say your offer is $36,000 and you take a $3,000 cash advance up front. At closing, you receive the remaining $33,000.

Of our customers who have sold their structured settlement payments, 44% used their lump sum to purchase a home or make a down payment, according to CSF's internal transaction data (2011 to 2026). That is the most common use we see, followed by paying off high-interest debt and covering medical expenses. Whatever your reason, the process is the same. We cover every step in detail in our guide on how structured settlement sales work.

Have questions about what your payments are worth? Call us at (800) 317-3769. That gets you a direct line to our team, not a call center. A quote takes a few minutes and there is no obligation.

Companies That Buy Structured Settlements

Companies that buy structured settlements fall into two categories: direct funders who purchase payments with their own capital and brokers who shop your deal to other companies for a commission. Our dedicated guide to structured settlement buyers covers each of the major firms in 2026 plus the evaluation criteria you can apply in one sitting.

If you are comparing structured settlement companies right now, you are already ahead of most sellers. We see the same pattern over and over: someone accepts the first offer that lands in front of them, and they leave thousands of dollars on the table. The fact that you are researching companies means you are doing this the right way.

The first thing to understand is the difference between a direct funder and a broker. A direct funder originates and funds the transaction using its own network of financial partners. A broker collects your information, shops it to multiple funders, and takes a cut. That middleman cost comes directly out of your lump sum. When you call a company, ask one question before anything else: "Are you a direct funder, or do you broker deals to other companies?"

What to Look for in a Structured Settlement Company

| Factor | What It Tells You |

|---|---|

| BBB rating and complaint history | Check the company's Better Business Bureau profile for its rating and any unresolved complaints |

| Years in business | Longer track records mean more experience with court filings, issuers, and state-specific requirements |

| Direct funder vs. broker | Direct funders cut out the middleman, which typically means a larger lump sum for you |

| Attorney involvement | Companies with attorneys on staff can handle legal filings in-house rather than outsourcing |

| Written disclosure statement | Required by your state's SSPA. Every legitimate buyer provides one before you sign anything |

| Cash advance availability | Not every company offers advances on pending transactions. If you need money before court approval, ask |

CSF has closed more than 3,900 structured settlement transactions across all 50 states since 2011. We are direct funders with attorneys on staff. Our BBB profile is public, our track record is verifiable, and 99% of our customers had previously worked with another structured settlement company before choosing us, according to CSF's internal customer data (2024 to 2026). That number tells you something about what happens when people compare.

Get quotes from at least two or three companies before making a decision. We say that because we know what happens when people compare. They usually come back to us. Our structured settlement company comparison breaks down the major buyers side by side so you can evaluate each one on the facts.

Issuers We Have Worked With

CSF has purchased structured settlement payments funded by every major annuity issuer in the United States, with more than 3,900 completed transactions since 2011.

Your annuity issuer is the insurance company that funds your structured settlement payments. When you sell, the issuer has to process the transfer paperwork after the court approves the transaction. Each issuer has its own internal process, its own Verification of Benefits (VOB) turnaround times, and its own transfer paperwork requirements. We know all of them because we have worked with all of them.

Here are the issuers we work with most frequently, based on CSF's completed transaction data from 2011 to 2026.

| Annuity Issuer | CSF Transactions |

|---|---|

| American General / Corebridge | 400+ |

| MetLife | 390+ |

| Prudential | 345+ |

| Symetra | 240+ |

| Allstate / Everlake | 210+ |

| Genworth | 170+ |

| Pacific Life | 155+ |

| Talcott Resolution (formerly Hartford) | 155+ |

| John Hancock | 150+ |

| New York Life | 140+ |

Why does the issuer matter to you? Because each one moves at a different speed after court approval. Some issuers process transfer paperwork in five to seven business days. Others take two to three weeks. We know which issuers move fastest, which ones require specific forms, and which ones have quirks in their process that can cause delays if you do not know about them in advance.

For example, Allstate (now Everlake) enforces a six-month cooldown period from the date you file your petition. John Hancock applies a similar six-month window from the date of the court order. MetLife restricts partial payment transfers in more than 24 states under the NCOIL "divide periodic payment" provision. These are the kinds of details that can catch sellers and less experienced buyers off guard.

We know each issuer's internal process, their VOB turnaround times, and their transfer paperwork requirements. That experience translates directly into faster closings and fewer surprises for you. Our full issuer guide covers each company in detail, including VOB phone numbers, entity structures, and what to expect during the transfer.

Advantages of Keeping Your Structured Settlement

Selling is not the right move for everyone, and we will never pressure you into it. Before you decide, consider what you are giving up:

- Typically tax-free income. Under IRC Section 104(a)(2) (opens in a new tab), payments from personal physical injury settlements are generally tax-free, including the investment growth. Non-physical claims may be taxable. We recommend talking to a tax professional, and we go deeper into this topic in our tax implications guide.

- Beneficiary protection. If you pass away during a guaranteed payment period, your designated beneficiary continues receiving the remaining payments.

- Market-insulated. Your payments are unaffected by stock market drops or economic downturns.

- Built-in growth. Many settlements include a cost-of-living adjustment (COLA) of 1 to 4% annually, so your payments increase over time.

Our team will walk you through the trade-offs so you can weigh the numbers yourself. We want to earn your business, not pressure you into a sale before you are ready.

What is a disadvantage of a structured settlement?

The main disadvantage is the lack of flexibility. Once your payment schedule is established, you cannot change it to access a larger sum when you need it, unless you sell some or all of your future payments to a licensed buyer. Fixed payments may also not keep pace with inflation over time. That said, this rigidity is also what makes structured settlements effective at providing long-term financial security. If your circumstances have changed and you need cash now, selling your payments is a legal option in all 50 states.

Why Court Approval Protects You

Every structured settlement transfer in the United States requires court approval. This is not red tape. It is the single most important protection you have as a seller, and both federal and state law enforce it.

Under 26 U.S.C. § 5891 (opens in a new tab), any company that acquires structured settlement payment rights without court approval faces a 40% federal excise tax on the entire difference between the face value of the payments and the purchase price. That tax is so large that it effectively forces every legitimate buyer to go through the court process. The statute was enacted in 2002 as part of the Victims of Terrorism Tax Relief Act and has remained unchanged since. Federal courts have called the court approval requirement the "cornerstone" of both state and federal law in this area. For the verbatim statutory text with subsection-by-subsection annotation, see our annotated IRC § 5891 page.

What does the court actually do? A judge reviews the specific terms of your deal and must find that the transfer is in your best interest, taking into account the welfare of your dependents. The judge looks at why you want to sell, what you plan to do with the money, whether you have other income, and whether the financial terms are fair. If the judge is not satisfied, the petition is denied. We have seen it happen to other companies that file incomplete petitions or offer terms the court considers unreasonable.

The court process also protects you from a specific risk that most sellers do not think about. In a 2024 Ninth Circuit case, approximately 2,000 payees sued their annuity issuer for inducing them into factoring transactions at steep discounts. The issuer was both the company making the structured settlement payments and the company buying those payments back. That dual role created a conflict of interest that the payees alleged was not adequately disclosed. One plaintiff sold $695,000 in life-contingent payments for $18,609.

CSF is an independent third-party buyer. We do not issue the annuities we purchase. We have no pre-existing relationship with you and no financial incentive other than offering you a competitive price for your payments. When you work with an independent buyer, the court approval process functions the way it was designed: as an objective check on the fairness of the deal, not as a formality rubber-stamping a transaction between you and the company that already controls your payment stream.

One more thing worth knowing: § 5891 also preserves your tax-free status. If your structured settlement payments are tax-free under IRC § 104(a)(2) (personal physical injury), that treatment carries through the factoring transaction. Selling your payments does not convert tax-free income into taxable income. For a deeper walkthrough of how § 5891, § 104(a)(2), qualified assignments under IRC § 130, and the White v. Symetra conflict-of-interest precedent fit together, read our federal tax rules guide.

Cities We Serve in Depth

We work with customers nationwide, but four metro areas account for the largest share of our recent transactions. Each city page covers the local court process, typical timelines, and the courthouses our paperwork passes through.

- Chicago, IL. Cook County Circuit Court process, the highest-volume jurisdiction we file in.

- Dallas, TX. Dallas County process under the Texas SSPA (Tex. Civ. Prac. & Rem. Code Ch. 141).

- New York City. Five-borough Supreme Court filings, prime + 5% discount-rate cap.

- Phoenix, AZ. Maricopa County Superior Court, fast turnaround on uncontested petitions.

If you are weighing CSF against a specific competitor, our Peachtree Financial vs. CSF comparison walks through the side-by-side on pricing transparency, services, court filing experience, and track record.

Why Choose CSF?

We have been doing this for more than 15 years. Most customers who come to us after shopping around tell us they wish they had called us first. Here is why:

- Transparent pricing. The amount we quote is the amount you receive. Not a penny less.

- 4,000+ transactions closed. Our team has originated and funded thousands of annuity, lottery, structured settlement, and probate advance transactions across nearly every state.

- We handle everything. Court filings, legal paperwork, scheduling, insurance company coordination. You sign the documents and show up to the hearing. That is it.

- Cash advances available. Need money before court approval? We offer advances on pending transactions, often the same day you accept an offer.

- Direct funders. We are not a broker. We fund deals directly with our own network of financial partners, which means more cash in your pocket.

- Full disclosure. Every quote includes a written disclosure statement so you understand exactly how the numbers work before you sign anything.

The fastest way to find out what your payments are worth is to call us at (800) 317-3769 or fill out the form on this page. There is no cost, no obligation, and no pressure. If you are an heir waiting on an estate rather than a settlement recipient, our probate advance program may be a better fit.

What Our Customers Say

“Catalina Structured Settlements offers the best rates around, and my experience with them was by far the smoothest yet. They maintained consistent communication throughout the process, ensuring I was always informed. I had the pleasure of working with Ian as my representative, and I can confidently say this company prioritizes helping customers without resorting to aggressive sales tactics, a refreshing change after my experience with JGW.”

Lawrence R.

“I completed my deal with Catalina structured funding and they did me good. I worked with James and he quoted me more money than two other companies. I am recommending them to my other family members that may want a lump sum as well because they got me the most money.”

J T.

“Honestly worked with them twice and Ryan has been amazing. The owner Chris Milton was just as nice and very attentive to my needs! I would recommend 10/10. If I do another transaction I will be sure to go back!”

Fatesha B.

Get a No Obligation Lump Sum Quote

Ask about a same day cash advance

Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.

Calculate the Value of Your Payments

Tell us about your payment stream and we will get back to you with an estimate.

Frequently Asked Questions

How long does it take to sell my structured settlement?

Do I need a lawyer to sell my structured settlement?

Will I have to pay taxes on my lump sum?

Can I sell just a portion of my payments?

How much cash will I receive for my structured settlement?

Why does a judge have to approve the sale?

What is a life contingent structured settlement payment?

Can I get a cash advance while waiting for court approval?

What if other companies have already given me lower quotes?

Can I use the money from my structured settlement to buy a home?

Get a No Obligation Lump Sum Quote

Ask about a same day cash advance

Structured Settlement Services by State

CSF serves customers nationwide. Select your state for local information, laws, and a free quote.