Transferring Property After a Death Without a Will in California

Last updated:

When a California resident dies, property transfers through one of four routes. Three simplified paths avoid full probate, and full probate handles everything else. Here is how each works, with the 2026 thresholds.

This content is for informational purposes only and does not constitute legal advice. Laws vary by state and are subject to change. Consult a qualified attorney for guidance on your specific legal situation.

When a California resident dies, their property transfers through one of four routes. Three of them are simplified paths that avoid full probate entirely, and the fourth is full probate itself, the court-supervised process that handles everything the simplified paths do not. Which route applies depends on what the estate owns and what it is worth, not on whether the person left a will.

Below, we explain what happens to property when someone dies in California, what changes when there is no will, the three paths that avoid full probate, when full probate is required, the assets that skip probate altogether, and what each route costs and how long it takes.

How Property Transfers After a Death in California

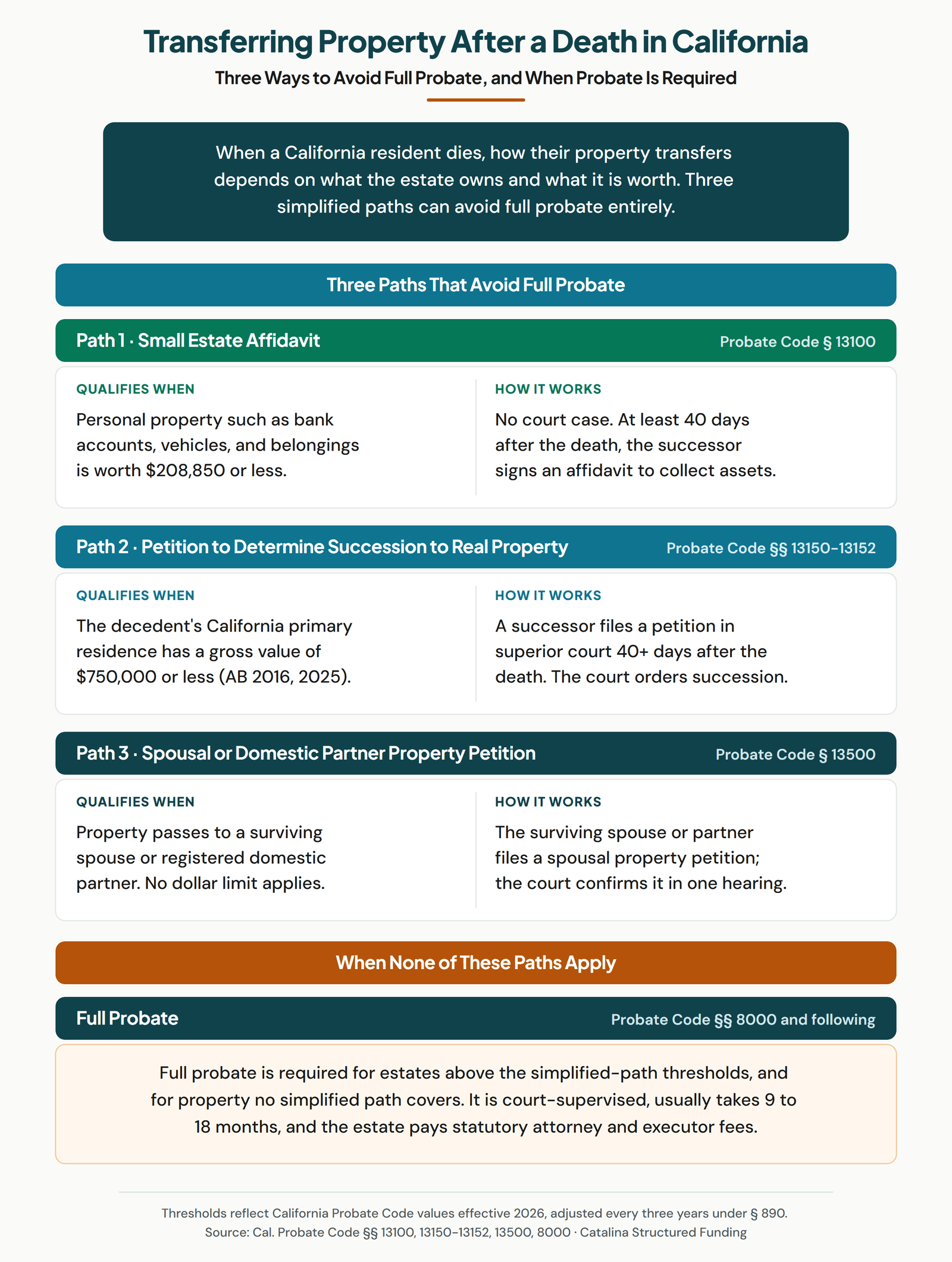

California property transfers after a death through a small estate affidavit, a real-property succession petition, a spousal property petition, or full probate. The first three are faster and cheaper. Full probate is the fallback when nothing else fits.

The deciding factors are simple. How much is the estate's personal property worth? Is there real estate, and what is it worth? Does the property pass to a surviving spouse? Answer those three questions and the route is usually clear. The chart above maps the whole decision, and the rest of this guide walks through each route in detail.

One thing to set straight at the start. Many people assume that dying without a will automatically triggers a long, expensive probate. It does not. The transfer route depends on the estate's size and makeup, and a no-will estate can use the same simplified paths as an estate with a will.

First Question: Is There a Will, and Does It Matter?

Whether there is a will changes who inherits, but it does not change which transfer route the estate uses. Those are two separate questions, and confusing them is the single most common mistake we see California families make.

If there is a valid will, it names who receives the property. If there is no will, the estate is intestate, and California Probate Code §§ 6400 through 6402 set a fixed order of who inherits: the surviving spouse and registered domestic partner first, then children, then parents, then more distant relatives. Our guide to California intestate succession walks through that order in full, including the community-property rules that make California different from most states.

Once you know who inherits, the transfer route is a separate decision driven by dollar values and asset types. A $300,000 all-cash estate with a will and a $300,000 all-cash estate with no will use the exact same paths. So when someone searches for how to transfer property after a death without a will, the honest answer has two parts: intestate succession decides the who, and the routes below decide the how.

There is also a middle case worth knowing about. A will can be valid but still fail to dispose of every asset, often because the person acquired property after signing the will and never updated it. The assets the will covers pass under the will, and the assets it misses pass by intestate succession. The four transfer routes apply either way, so a partially intestate estate is handled with the same procedures as any other.

The Three Paths That Avoid Full Probate

California offers three simplified procedures that transfer property without a full probate administration: the small estate affidavit, the petition to determine succession to real property, and the spousal property petition. Each has its own statute, its own threshold, and its own process.

These paths exist because full probate is slow and expensive, and the Legislature decided that smaller and simpler estates should not have to bear that cost. They are not loopholes. They are the routes California law intends most ordinary estates to use. The three sections that follow cover each one.

Path 1: The Small Estate Affidavit (§ 13100)

The small estate affidavit lets a successor collect a decedent's personal property without any court case when the estate's personal property is worth $208,850 or less. It is governed by California Probate Code § 13100 and the sections that follow it.

Personal property here means assets other than real estate: bank accounts, vehicles, brokerage accounts, and personal belongings. The successor waits at least 40 days after the death, signs a sworn affidavit stating that they are entitled to the property and that the estate qualifies, and presents the affidavit to whoever holds the asset, such as a bank. The bank releases the asset to the successor. No judge, no hearing, no filing fee.

The $208,850 figure is current as of 2026. It took effect April 1, 2025, and under Probate Code § 890 the small-estate dollar amounts are adjusted every three years, so the next change is April 1, 2028. One caution: the affidavit covers personal property only. Real estate needs Path 2.

One detail trips families up. The $208,850 limit counts only the estate's probate personal property. Assets that pass outside probate, such as a pay-on-death bank account, a retirement account with a named beneficiary, or anything held in a living trust, do not count toward the limit at all. An estate that looks large on paper can still qualify when most of its value sits in beneficiary-designated accounts and only a modest amount of cash and belongings would otherwise go through probate. Add up the probate personal property by itself before deciding this path is closed to you.

Path 2: Petition to Determine Succession to Real Property (§§ 13150-13152)

This path transfers a decedent's real estate without full probate when the property qualifies. For a decedent's primary residence, the gross value must be $750,000 or less, the threshold California created in Assembly Bill 2016, effective April 1, 2025.

The procedure is a court petition rather than a simple affidavit. A successor files a petition to determine succession to real property in the superior court of the county where the property sits, at least 40 days after the death. The court reviews the petition and, if the property qualifies, issues an order establishing who now owns the real estate. There is a hearing, but there is no full administration, no personal representative running the estate for a year, and no statutory percentage fee.

AB 2016 was a significant change. Before April 1, 2025, the real-property thresholds were far lower, and many California families with an ordinary home had no choice but full probate. The $750,000 primary-residence threshold now keeps a large share of California homes out of full probate. A separate, smaller affidavit procedure under § 13200 also exists for real property of very low value, but the § 13151 primary-residence petition is the path that matters for most homeowners.

Path 3: Spousal or Domestic Partner Property Petition (§ 13500)

When property passes to a surviving spouse or registered domestic partner, the Spousal Property Petition under California Probate Code § 13500 confirms the transfer without full probate. This path has no dollar limit, which sets it apart from the other two.

The surviving spouse or partner files a spousal property petition in superior court. The court confirms that the identified property passes to or already belongs to the survivor, often in a single hearing. Because there is no value cap, a surviving spouse can use this path even when the estate is large, including a home worth well above the $750,000 figure that limits Path 2.

This is why a surviving spouse in California is often able to avoid full probate even for a substantial estate. The path covers both the survivor's existing community-property half and the share of the decedent's property that passes to the survivor under the will or under intestate succession. For married couples, it is frequently the cleanest route.

Even a simplified transfer path takes time, and full probate can run well over a year. If you are a California heir who needs cash before the estate settles, Catalina Structured Funding can advance a portion of your inheritance, with approval based on the estate rather than your credit. Call (800) 317-3769 for a free quote, or read more about California probate advances.

When Full Probate Is Required

Full probate is required whenever the estate does not fit a simplified path. In practice that means personal property worth more than $208,850, a residence worth more than $750,000 that does not pass to a surviving spouse, or any property that no simplified procedure covers.

Full probate is the court-supervised administration set out in California Probate Code § 8000 and the sections that follow, and it runs on a set of standardized Judicial Council forms that our California probate forms guide walks through. A personal representative is appointed, the estate is inventoried by a probate referee, creditors are given a window to file claims, debts and taxes are paid, and the court approves a final distribution to the heirs. The process typically takes 9 to 18 months, and longer when there is real estate to sell or a dispute among heirs.

Full probate also carries the statutory fees. The attorney is paid under Probate Code § 10810 and the personal representative under § 10800, both on the same graduated schedule of the estate's gross value. Our California probate fees guide breaks those numbers down with worked examples, and the California probate timeline guide covers how the months actually unfold.

Assets That Transfer Outside Probate Entirely

Some assets never touch any of the four routes above because they pass directly to a named person by their own terms. These non-probate assets transfer outside the probate system whether or not there is a will.

The common ones are:

- Living trust assets. Property held in a properly funded revocable living trust passes to the trust beneficiaries under the trust document, with no probate at all.

- Beneficiary-designated accounts. Life insurance, retirement accounts, and pay-on-death or transfer-on-death bank and brokerage accounts pass directly to the named beneficiary.

- Joint tenancy property. Real estate or accounts held in joint tenancy with right of survivorship pass automatically to the surviving owner.

- Transfer-on-death deeds. A recorded transfer-on-death deed passes the named real property to the named beneficiary outside probate.

This is why two heirs of the same person can have very different experiences. One named on a pay-on-death account may receive that money within weeks, while another waiting on the probate estate waits a year. If you are unsure which category an asset falls into, the estate attorney can tell you, and it is worth asking early.

The practical takeaway is to inventory the whole estate before choosing a route. List every asset, then mark which ones already have a named beneficiary, a survivorship feature, or a trust holding them. Those are settled and need no court procedure at all. What is left is the probate estate, and only that remainder is measured against the $208,850 and $750,000 thresholds in this guide. Mapping the estate this way often reveals that a simplified path was available all along, and that full probate was never actually required.

What Each Path Costs and How Long It Takes

The four routes differ sharply in cost and speed. The small estate affidavit is the fastest and cheapest, and full probate is the slowest and most expensive, with the two petitions in between.

| Route | Court Involvement | Typical Timeline | Cost |

|---|---|---|---|

| Small estate affidavit (§ 13100) | None | Usable 40 days after death | Lowest, no filing fee or statutory fee |

| Real-property petition (§§ 13150-13152) | One petition and hearing | A few months | A filing fee, no statutory percentage fee |

| Spousal property petition (§ 13500) | One petition and hearing | A few months | A filing fee, no statutory percentage fee |

| Full probate (§ 8000+) | Court-supervised throughout | 9 to 18 months or longer | Highest, statutory § 10810 and § 10800 fees plus costs |

Swipe to see all columns →

The cost gap is large. A simplified path on a qualifying estate can cost a few hundred dollars in filing fees. Full probate on a $1,000,000 estate carries roughly $46,000 in combined statutory attorney and executor fees alone. That difference is the reason it is worth checking carefully whether an estate qualifies for one of the three simplified paths before defaulting to full probate.

Which Path Fits Your Situation

Matching an estate to the right route comes down to a short series of questions. Work through them in order.

- Does the property pass to a surviving spouse or registered domestic partner? If so, the Spousal Property Petition under § 13500 is usually the route, and there is no value cap.

- Is the only real estate a primary residence worth $750,000 or less? The petition to determine succession to real property under §§ 13150-13152 can transfer it.

- Is the estate only personal property worth $208,850 or less? The small estate affidavit under § 13100 handles it with no court case.

- Is the estate larger than those limits, with no spousal transfer? Full probate is required.

An estate can use more than one path. A surviving spouse might use the spousal petition for the home and a small estate affidavit for the bank accounts. The routes are tools, and an estate often uses the combination that fits. When you are not sure, an estate attorney can confirm which procedures apply, and our probate advance calculator can estimate the numbers if full probate turns out to be the route.

A quick example shows how the routes combine. James, a widower, dies in California leaving a home worth $680,000, a $120,000 bank account, and a car. His daughter is the sole heir. The home qualifies for the Path 2 real-property petition because it is a primary residence worth less than $750,000. The bank account and the car are well under the $208,850 personal-property limit, so a small estate affidavit collects them. James's daughter never needs a full probate. Now change one fact. If the home were worth $900,000, it would exceed the Path 2 threshold, and with no surviving spouse to use Path 3, that home would have to go through full probate.

Common Mistakes When Transferring California Property

A few recurring errors cost California families time and money. Knowing them in advance is the simplest way to avoid them.

- Assuming no will means full probate. It does not. The simplified paths work for intestate estates too, and many families open a full probate they never needed.

- Valuing real estate at its equity instead of its gross value. Every California threshold and every statutory fee is measured on gross value, before subtracting the mortgage. A home with a large loan still counts at its full appraised price.

- Skipping the check for non-probate assets. Before opening any procedure, find out which assets already have a named beneficiary or a survivorship feature. Those transfer on their own and do not count toward the small-estate limit.

- Missing the 40-day wait. The small estate affidavit and the real-property petition cannot be used until at least 40 days have passed since the death. Acting too early gets the request rejected.

- Using the wrong path for the asset type. The small estate affidavit covers personal property only. Real estate needs the § 13150 petition, or for a surviving spouse the § 13500 petition. Mixing them up means starting over.

When the estate is genuinely complex, or when an heir is unsure, a short consultation with a California probate attorney is worth the cost. Guessing wrong is almost always more expensive than asking.

Frequently Asked Questions

How do I transfer property after death without a will in California?

First, intestate succession under Probate Code §§ 6400-6402 decides who inherits. Then the property transfers through one of four routes: a small estate affidavit for personal property up to $208,850, a court petition for a primary residence up to $750,000, a spousal property petition, or full probate. The right route depends on what the estate owns and what it is worth.

When is probate required in California?

Full probate is required when the estate does not fit any simplified path. That generally means personal property above $208,850, a residence worth more than $750,000, or property that does not pass to a surviving spouse. Estates below those lines, or property passing to a spouse, can usually avoid full probate.

What is the small estate affidavit threshold in California for 2026?

The California small estate affidavit threshold is $208,850 in personal property, effective April 1, 2025. Under Probate Code § 890 the figure is adjusted every three years, so the next change is April 1, 2028. The $208,850 amount applies to deaths on or after April 1, 2025.

Does property always go through probate if there is no will in California?

No. Dying without a will does not force a full probate. The same simplified paths, the small estate affidavit, the real-property petition, and the spousal petition, are available whether or not there is a will. Intestate succession decides who inherits, and the transfer route is a separate question driven by the estate's size and makeup.

Can a surviving spouse avoid probate in California?

Often, yes. A surviving spouse or registered domestic partner can use the Spousal Property Petition under Probate Code § 13500 to confirm that property passes to them, usually in a single court hearing. There is no dollar limit on this path, which makes it valuable even for large estates.

How long does each alternative-to-probate path take in California?

A small estate affidavit can be used 40 days after the death and involves no court case. The real-property and spousal petitions require a court hearing and typically take a few months. Full probate, by contrast, usually runs 9 to 18 months or longer.

If you are a California heir and the estate is heading into full probate, you may be waiting a year or more for your inheritance. Catalina Structured Funding can give you a free probate advance quote within 24 hours. Approval is based on the estate, not your credit, and the amount we quote is the amount you receive. Call (800) 317-3769 or request a quote on this page.

Sources

7 cited sources. Every authority below appears in the article above and was reviewed by our editorial team. See our editorial standards for our sourcing policy.

- StatuteCal. Probate Code § 13100 (Small estate affidavit for collection of personal property)

- StatuteCal. Probate Code §§ 13150-13152 (Petition to determine succession to real property, including the primary residence)

- StatuteCal. Probate Code § 13151 (Primary-residence succession petition, $750,000 gross-value threshold under AB 2016)

- StatuteCal. Probate Code § 13500 (Spousal or domestic partner property petition)

- StatuteCal. Probate Code § 890 (Triennial adjustment of small-estate dollar amounts, April 1, 2022 / 2025 / 2028)

- StatuteCal. Probate Code §§ 8000-8007 (Commencement of full probate administration)

- StatuteCal. Probate Code §§ 6400-6402 (Intestate succession order when there is no will)

Get a No Obligation Lump Sum Quote

Ask about a same day cash advance

Get a No Obligation Lump Sum Quote

A member of our team will reach out to you shortly.

Get a No Obligation Lump Sum Quote

Ask about a same day cash advance

Related Posts

New California Probate Laws in 2026 and What They Mean for Heirs

California lawmakers are advancing nine bills that change the state Probate Code in 2026. See what...

Is a Probate Advance Legit? What to Know Before You Apply

Probate advances are legitimate, and they are not loans. Here is how the non-recourse assignment...

Intestate Succession in Texas: Who Inherits

Texas Estates Code §§ 201.001-201.103 sets who inherits when someone dies without a will. The rules...